End-to-end ownership

I own products from discovery through rollout: problem framing, scope, acceptance criteria, UAT, launch coordination, and iteration.

Product Owner with 8+ years in fintech delivery across digital banking, payments, and integrations. I structure ambiguous system problems into scalable product workflows, then use AI-assisted tooling (Cursor, Kiro, agents) to reduce manual effort and accelerate discovery, specification, QA readiness, and release execution.

Product work across ACH, Positive Pay, SDK/API integrations, business banking, and self-service flows used in production banking environments.

Fast scan for recruiters, deeper signal for hiring managers.

I own products from discovery through rollout: problem framing, scope, acceptance criteria, UAT, launch coordination, and iteration.

I lead complex third-party and internal integrations across SDKs, APIs, and identity layers, aligning product, engineering, compliance, and operations to deliver stable, scalable releases.

I design pragmatic paths through core banking limitations with phased MVPs, then use Cursor, Kiro, and agent workflows to accelerate documentation, prototyping, and execution.

Ship what customers can trust now, while building the platform architecture needed next.

Selected initiatives that show how I frame hard product problems, make integration tradeoffs, and ship from definition through release.

Featured case study · Product Owner · ACH controls and exception workflows

Result: Established a scalable bridge from opaque rules-driven ACH handling to clearer exception-based decisioning with stronger user control, faster decision-making, and lower support ambiguity.

Problem: legacy ACH Positive Pay logic relied on hidden backend rule behavior, leaving institutions with limited visibility and inconsistent decisioning experiences for unmatched incoming ACH activity.

The legacy model did not behave like standard exception-first Positive Pay experiences. Users could not reliably see or action unmatched ACH items in a clear review workflow.

Core-system limitations restricted full redesign scope, compliance required auditable decision states, and rollout needed low-risk sequencing across active banking clients.

Incoming ACH activity is identified before it becomes an unclear customer-support issue.

Defined an MVP with a default blanket-block rule so inbound ACH items entered an exception queue immediately, then mapped decision states, posting rules, and audit events before backend changes.

Wrote Gherkin acceptance criteria, sequenced dependency tickets for rule creation and decision APIs, and ran implementation trade-off calls with core SMEs and engineers.

Increased clarity and control in ACH exception handling, reduced workflow ambiguity, and enabled a scalable path toward mature exception-first controls.

Why this mattered: it converted a hard-to-explain backend behavior into a clearer customer-facing control model that teams could trust and scale.

Case study available on request.

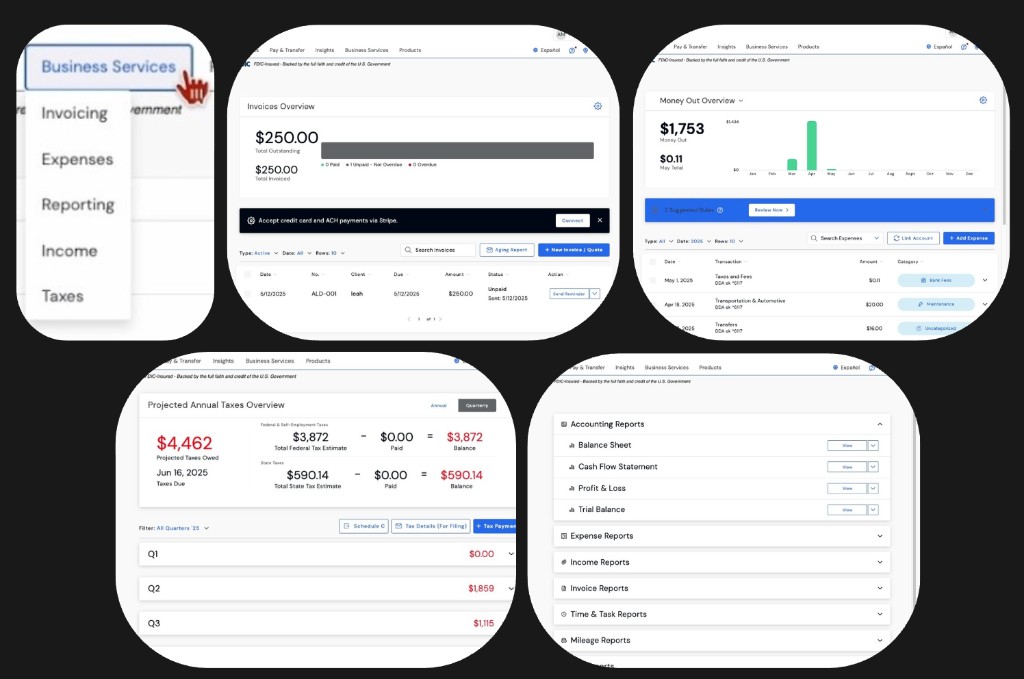

Product Owner · Phased rollout across web and mobile

Business users lacked integrated tools for invoicing, expense tracking, income management, tax estimation, and reporting.

Result: Enabled business users to complete invoicing, expense tracking, tax estimation, and reporting directly in digital banking, decreasing reliance on external tools and fragmented workflows.

Owned phased delivery of Hurdlr SDK modules (invoicing, expenses, income, tax, reporting), including API handoffs, account mapping, entitlement rules, and web/mobile parity decisions.

Enabled faster delivery of business-banking capabilities and a cleaner rollout model for future premium features.

Selected screens from the Business Services suite (invoicing, expenses, taxes, reporting) integrated into digital banking.

Case study available on request.

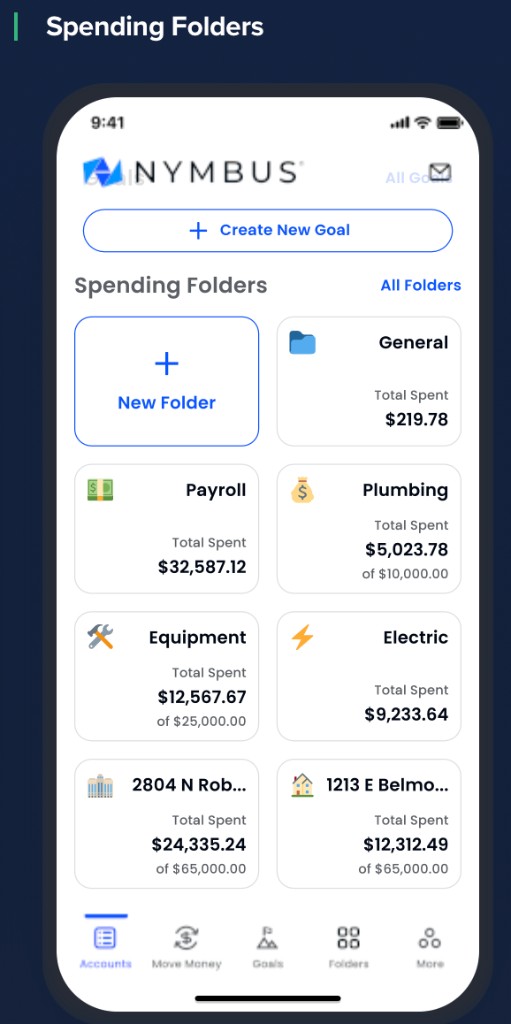

Product Owner · Rebrand and platform evolution

"Spending Folders" supported debit categorization only, limiting business value and creating unclear feature positioning.

Result: Enabled bidirectional transaction organization, streamlined categorization workflows, and reduced ambiguity in folder-based reporting context.

Reframed and redesigned the feature as "Transaction Folders" with credit/debit support, metadata tagging rules, bulk/manual assignment workflows, and linkage points into Check Positive Pay exceptions.

Increased utility by enabling richer organization, clearer reporting context, and stronger alignment with adjacent risk controls.

Transaction Folders redesign on mobile.

Case study available on request.

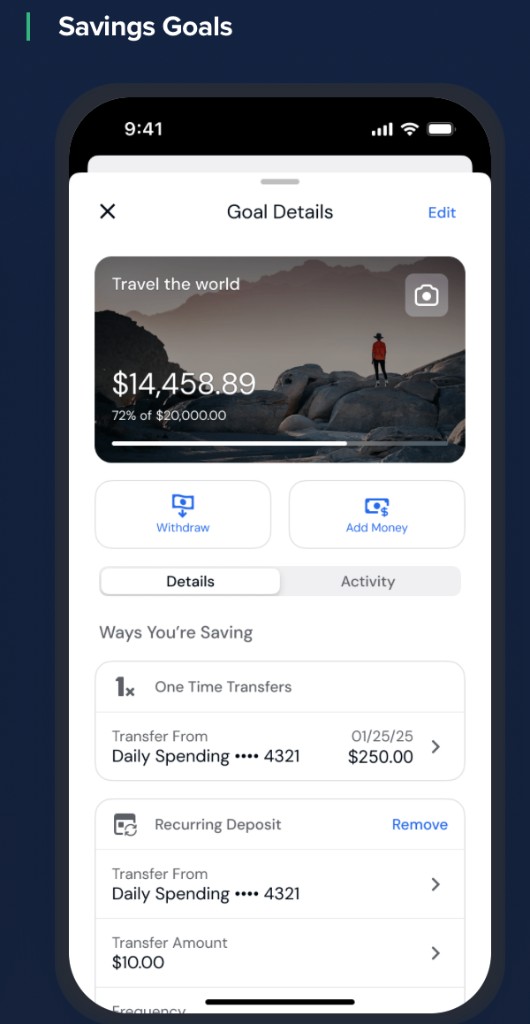

Product Owner · Mobile goals experience

Goal tracking needed a clearer, action-first mobile experience so users could monitor progress and manage contributions without leaving digital banking.

Result: Increased visibility into goal progress and accelerated contribution actions for one-time and recurring deposits.

Owned redesign scope for goal detail workflows, including progress visibility, one-time transfer and recurring deposit management, and activity context in a single screen hierarchy.

Improved goals clarity with clearer balance-to-target progress and faster contribution actions.

Savings Goals redesign on mobile.

Case study available on request.

Product Owner · Web & mobile

Stop payment requests were manual and support-heavy, creating unnecessary friction for users and operations.

Result: Shifted stop-payment initiation into self-service flows that reduced manual handling, enabled faster action, and improved user control during time-sensitive events.

Led self-service design and delivery for single and range-based stop requests with account-level vs global fee configuration, disclosure rules, confirmation states, and audit trail requirements across web and mobile.

Reduced operational dependency on manual channels, increased customer control, and established reusable self-service patterns.

Stop payment screens available on request.

Case study available on request.

Product Owner · Mobile SDK and white-label delivery

Built a consistent in-app messaging experience across multiple client environments with distinct branding, routing, and service requirements.

Result: Delivered a reusable messaging integration model that streamlined white-label deployment setup, routing behavior, and customer context handoff while accelerating multi-client rollout readiness.

Owned NICE CXone mobile SDK setup for a white-label model: channel configuration per FI, brand/theme controls, bot-to-agent routing, customer metadata context passing, post-chat survey behavior, and language handling.

Enabled scalable messaging with preserved customer context and more consistent operations across deployments.

Case study available on request.

Product Owner · Third-party platform integration

Integrated a third-party commercial credit card platform into digital banking experiences with complex servicing and operational requirements.

Result: Enabled role-aware card servicing and controls with a rollout model that balanced API complexity, entitlement accuracy, and operational reliability while improving day-to-day servicing clarity.

Defined API-driven servicing flows for card controls, spend limits, freeze/unfreeze actions, and role-based permissions for admins, operators, and viewers; sequenced implementation and rollout cutovers.

Enabled clearer card controls, better servicing pathways, and reliable rollout execution.

Case study available on request.

I use AI directly in product execution to reduce manual effort and speed delivery.

This workflow improves iteration speed and decision quality while keeping delivery disciplined in regulated fintech environments.

Impact-focused timeline across product delivery and banking operations.

Mix of product craft, delivery, and banking depth.

Jefferson State Community College — May 2014

Knowledgehut — June 2022

Interested in product leadership roles with meaningful AI leverage.

Additional implementation details and integration architecture case studies are available on request.

Want a 60-second walkthrough?